Policy brief: Economic forecasts just one piece of the revenue puzzle

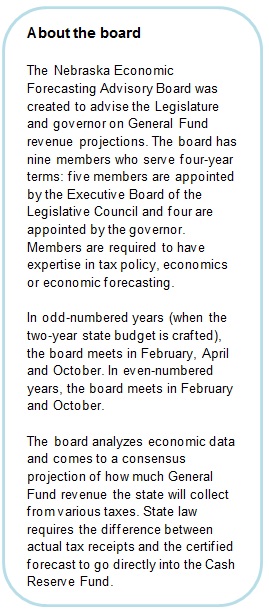

The next Nebraska Economic Forecasting Advisory Board meeting is Friday and the board’s action will likely cause a reaction in the State Capitol. Oftentimes, the board’s actions are followed by calls for tax cuts or increased spending.

Regardless of what the board decides, there are factors other than the projections to consider when making state fiscal policy decisions.

Nebraska Economic Forecasting Advisory Board reports are often followed by calls for tax cuts and increased spending. But the reports are just one part of the state’s overall budget picture, which means there are several other factors to consider when making fiscal policy. (Photo provided courtesy of the Unicameral Information Office.)

Importance of the cash reserve

The Government Finance Officers Association recommends that states have two months’ worth of budget — or the equivalent of 16.7 percent of the General Fund — in the cash reserve. Nebraska’s cash reserve is now at $708 million – right at 16.7 percent of the General Fund.

Based on current revenue projections, the cash reserve will need to reach $770 million by FY 2016-17 to meet that two-month recommended minimum. And it is on pace to meet that amount, currently projected to reach $769 million.[1]

Nebraska reached the recommended minimum only once, in FY09, just in time for the worst of the revenue losses from the Great Recession, and we dipped into those savings to help support state services during the next few years. There is a recession every 6.6 years, on average.[2]

The Pew Charitable Trusts, acknowledging that revenue volatility is normal, cautioned recently that periods of unexpected high revenue could easily be followed by years of low revenue, prompting service cuts or increased taxes to make ends meet.

Pew said state tax collections appear to have become more volatile over the past decade, creating new challenges for policymakers in long-term budgeting. Pew cautioned about misinterpreting positive revenue upticks as a trend and that lawmakers need to understand their state’s unique patterns of volatility.” [3]

Key Questions

Before reaching policy conclusions based on a new or revised revenue forecast, residents and policymakers should consider the forecast in the context of long-term historical trends and the broader economy. Below are some of the questions that can help provide that perspective.

What are other indicators of economic growth?

Economic information to consider might include reports that the LFO and Department of Revenue (DOR) provide using data from Global Insight, Moody’s and other sources such as Federal Reserve Bank. Personal Income data are published quarterly by the Bureau of Economic Analysis. Also of use are “Nebraska Monthly Economic Indicators” published by the University of Nebraska-Lincoln’s College of Business Administration.

Are there temporary factors at play that might explain changes in the forecast?

Sometimes, an increase or decrease in the forecast may be triggered by unusual events that are not part of a long-term trend. A harsh winter or a summer drought may drive revenues down temporarily, for example. Or as happened in recent years, uncertainty about federal policy may lead people to change their tax planning practices.

Which tax types are driving the changes and why?

A change in the sales tax forecast, for example, indicates people are spending more and therefore increased sales for Nebraska businesses. An income tax change, on the other hand, may indicate a stronger Nebraska economy or may indicate a booming stock market driven by non-Nebraska companies. These details must be considered to fully understand a change in the forecast.

How significant is the forecast change?

The total General Fund budget is more than $4 billion, so changes to the forecast that sound quite significant may actually be very small relative to the full budget.

Conclusion

The board’s projection is but a piece of a bigger budget picture – a tool to be used in decision making — but the state needs to take all economic factors into account when making fiscal policy decisions. Doing otherwise could have negative ramifications for our schools, communities and economy.

Download a printable PDF of this analysis.

[1] Numbers based on October 2014 projections, which will be revised February 28, 2015.

[2] “U.S. State Fiscal Recoveries Vary As Crucial Budget Choices Loom,” Standard & Poor’s Global Credit Portal, April 23, 2014.

[3] “Managing Uncertainty, How State Budgeting Can Smooth Revenue Volatility,” The Pew Charitable Trusts, Feb. 2014.