Revenue reductions enacted by Nebraska lawmakers in recent years rank among the deepest cuts in the nation, shifting billions in public funds away from key investments and toward tax cuts.

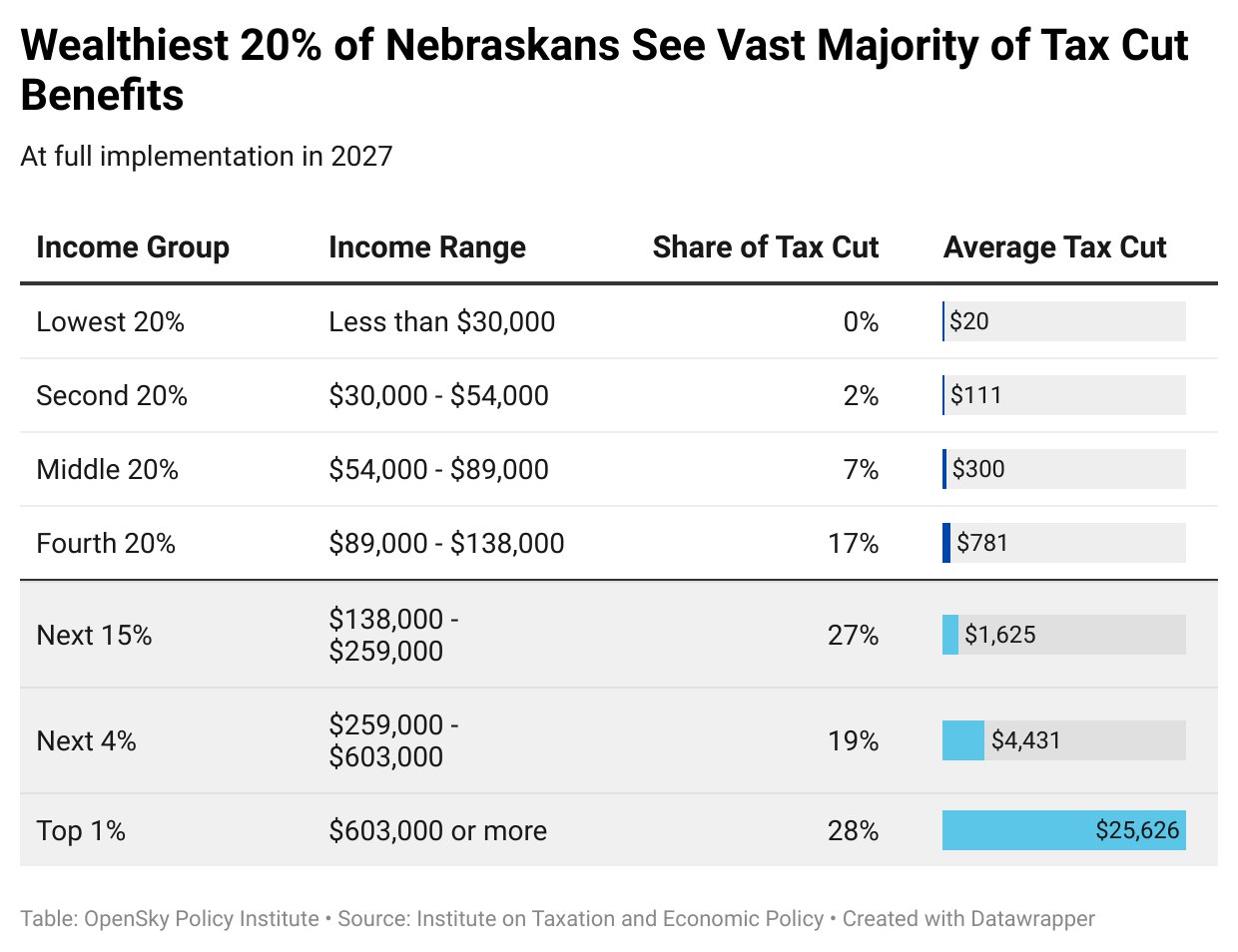

Personal and corporate income tax cuts passed in 2021, 2022 and 2023 have cost only $77 million thus far but will grow more expensive over time, reducing state revenues by nearly $3.1 billion over the next five years while the benefits of those tax cuts are targeted predominantly to corporations and the wealthiest Nebraskans.

That’s a decline of general fund revenue of 7.6%, the sixth steepest reduction among the 26 states to enact cuts to personal or corporate income taxes, or both, over the past three years. according to a report by the Center on Budget and Policy Priorities. These permanent cuts built on temporary budget surpluses will make it difficult for lawmakers to sustain what the state invests currently in schools, health care and public safety.

That’s a decline of general fund revenue of 7.6%, the sixth steepest reduction among the 26 states to enact cuts to personal or corporate income taxes, or both, over the past three years. according to a report by the Center on Budget and Policy Priorities. These permanent cuts built on temporary budget surpluses will make it difficult for lawmakers to sustain what the state invests currently in schools, health care and public safety.

The $1 billion revenue loss projected in 2028 equals roughly what Nebraska spends annually on its entire Medicaid program, which serves over 350,000 low-income children and adults, seniors and people with disabilities. With less revenue, policymakers won’t have the resources to invest in stable, affordable housing and high-quality child care vital to the hard-working Nebraskans who are the engine to the state’s economic growth.

Lawmakers, by putting years between the tax policy decisions made now and the likely harmful and unpopular effects to come, undermine accountability and pass on difficult decisions to future legislatures when faced with an economic downturn. In the decade after the Great Recession, when 18 states cut their personal or corporate income tax rates, those decisions eventually led to higher tuition rates at public colleges and universities, cuts in K-12 school funding and contributed to a slower economic recovery.

The Center on Budget Policy and Priorities report notes that while a majority of states cut tax rates in the past three years, others chose a different path. For example, Washington established a new tax on capital gains received by the wealthiest 0.2% of taxpayers that’s expected to raise at least $500 million in new annual revenue for child care and school improvements.

In Kansas, where budget-busting revenue reductions in the early 2010s remain a warning sign for tax-cutting states, the governor and lawmakers rejected a flat-tax proposal estimated to cost nearly $1.4 billion over just three years.

Structural deficits for Nebraska are already projected in the years to come. When senators reconvene in January, they will need to look at how to keep revenues on a sound footing to ensure all Nebraskans can thrive in the years to come.

{kind=link}