Frequently asked questions about LB 280’s impact on school finance

LB 280 would protect funding for K-12 education, while reducing Nebraska’s heavy reliance on property taxes to fund schools. To accomplish this, the bill would:

- Reduce agricultural land valuation from 75 percent to 65 percent for K-12 funding formula purposes only. This would direct more state aid to school districts with high agricultural land values without reducing revenue for schools or other local services. Many schools that don’t get equalization aid now would under this change.

- Expand the resource calculation of the school aid formula by adding a local income tax tied to a reduction in property taxes. This would assess a community’s ability to pay based on property and income wealth, would lower property taxes across the state and would keep the local income tax revenues with the local school district. Those school districts with unmet needs can raise additional dollars by increasing their local income tax rate by a supermajority vote of the school board or a majority of district voters.

- Create a per-student aid component. The proposal would provide a per-pupil amount of $500 to every district, regardless of whether a school receives equalization aid or not.

Below we answer frequently asked questions regarding LB 280’s impact on school finance.

1. How does the school-funding surtax (local income tax component) work?

LB 280 creates a school-funding surtax, which is the local income tax component. A surtax is calculated by multiplying a person’s state individual income tax liability by a set percentage — the rate set in LB 280 is 19.4% of state income tax liability. As a very simplistic example, if a person owes $1,000 in state income tax, the school-funding surtax would be an additional $194. Alternatively, if a person owes no state income tax, he or she pays no school-funding surtax either. This surtax would be paid at the same time as state income taxes and on the same form. For Nebraska residents & partial-year residents, the revenue from the surtax will be distributed back to the taxpayer’s home school district. These surtax revenues would be counted as district resources for the purposes of the TEEOSA formula. For non-residents, the revenue from the surtax will be owed to the state and credited to the General Fund.

2. How does LB 280 change the financial resources available to my school district?

LB 280 changes the mix of revenue sources available, but it does not change the amount of resources available to school districts. LB 280 expands the resources calculation by creating a school-funding surtax (local income tax component) that would be coupled with a reduction in property taxes. Adding the surtax revenue — while maintaining existing budget growth limits and reducing the maximum levy — would lower property taxes for all districts. The expanded resources calculation in TEEOSA means each district’s ability to pay would now be a more holistic accounting of their property and income wealth combined. Equalization aid would be distributed to districts with low amounts of resources relative to their needs. (View examples of how this proposal would impact 4 school districts.)

3. What is the local school board’s role in relation to the school-funding surtax provision in LB 280?

The base school-funding surtax rate of 19.4% is applied in all districts and is not optional. To implement this school-funding surtax component will require no action from the school board. However, the bill does provide an option for school boards to increase the school-funding surtax rate up to a maximum of 29.9% with a supermajority vote of the board or a majority of district residents. School boards still set their own local property tax levies.

4. What is the impact on equalization aid?

Equalization aid would still be distributed to districts that have lower resources in relation to their needs, but that calculation of resources would include both property and income wealth. LB 280 would increase state aid in 222 of Nebraska’s 245 school districts — more than 90 percent of districts. Twenty-three districts would receive less state aid because they have high incomes that had previously not been taxable by local schools or considered in the state aid formula. Although these 23 districts would lose state aid, their overall level of funding would be held harmless because of the additional revenue they would collect through the school-funding surtax.

5. How does LB 280 change my district’s piece of the education funding “pie”?

If we talk about education funding as a pie, LB 280 is a new recipe. Looking at funding for education (including all state revenue sources currently available to schools), schools will have the same size piece of pie available to them under LB 280 as they do currently. However, the proportion of ingredients in their piece of the pie may change under LB 280. New ingredients in the LB 280 pie include: school-funding surtax revenue, per-student aid, and an injection of new revenue from the non-resident school funding surtax to the General Fund. Property taxes make up a smaller share of the total pie and a smaller portion in every district. The equalization portion is still targeted to districts with low amounts of resources relative to their needs.

6. Does this proposal address allowances or the “needs” side of the TEEOSA formula?

No. LB 280 only makes changes to the “resources” side of TEEOSA. It does not change the “needs” side, nor does it change the fundamental “needs minus resources = equalization aid” equation in TEEOSA.

7. What is the proposed timeline for implementation, if LB 280 is passed?

Under LB 280, the school-funding surtax (local income tax) will be collected beginning in 2016. The revenue from the school-funding surtax for 2016 will be available to school districts in 2017. The Tax Commissioner shall determine the total school-funding surtax owed to each district and shall distribute the amount to the school district on or before July 1, 2017 and July 1st each year thereafter. School-funding surtax revenue shall be included in formula system resources in school fiscal year 17-18 and each year thereafter. School districts shall notify the Tax Commissioner by August 1st of each year of the school district’s school-funding surtax amount to be imposed for the following year. The reduction in the maximum property tax levy in LB 280 is reduced gradually – 95 cents per $100 of taxable valuation of property subject to the levy in FY17-18, 90 cents in FY18-19, 85 cents in FY19-20, and 80.5 cents in FY20-21 and each year thereafter.

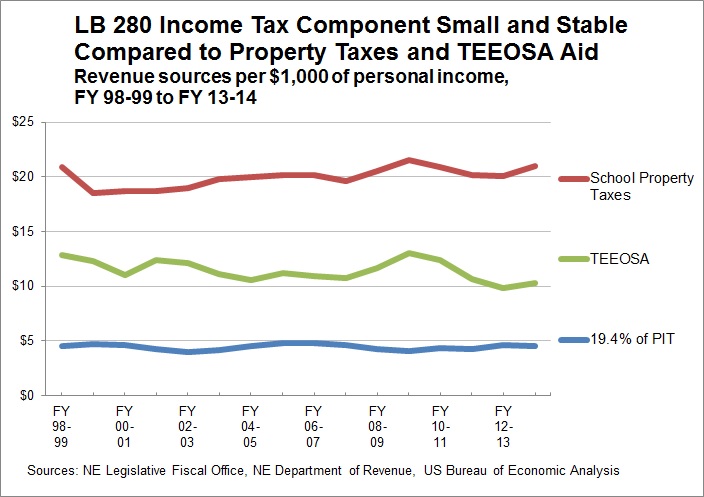

8. Aren’t property taxes the most stable source of revenue? Won’t adding income as a revenue source make the school funding system less stable?

Ideally, state and local revenue comes from a balanced mix of property, income, and sales taxes – sometimes referred to as a “three-legged stool.” LB 280 maintains stable funding for schools and other services and spreads taxes more equitably. Nebraska’s reliance on property taxes to fund K-12 education has created a “wobbly stool,” which could be stabilized by additional sources of revenue. We can’t avoid the ups and downs of the economy or tax revenues, but the best defense against those fluctuations is to maintain a mix of different taxes and a healthy rainy day fund. Furthermore, relying so heavily on property taxes to fund schools leaves us vulnerable as well. If we should experience a drop in the high agricultural land values that have facilitated our shift to more property taxes, we will be faced with the need for more state aid or cuts to our schools. Also, while income taxes are considered a somewhat more volatile revenue source than property taxes, the income tax component in LB 280 is too small to significantly increase volatility in the school funding system. The average swing in school property taxes from year to year is about $65 million, while the average swing for 19.4 percent of income taxes — the percentage taxed in LB 280 — has been about $20 million. Being able to tax both property and income will make school funding more stable, not less.

{kind=link}

9. Is school spending driving the increases in property taxes?

Total school spending as a share of the economy has actually gone down, decreasing about four percent from FY 98-99 to FY 12-13. The growth in school property taxes has been primarily driven by state aid reductions and growing property values. School districts are subject to a spending limit, a limit on cash reserves, and a property tax levy limit – all of which serve to significantly restrict school district spending and budget flexibility. The spending limit restricts the amount a school’s budget can grow from year to year to 2.5 percent, although the Legislature is allowed to annually change the growth rate. The amount of money that school districts can hold in reserve from year to year is limited. School districts have a maximum levy limit of $1.05 per $100 of property value (with a few exceptions), unless they have obtained a voter-approved levy override. These restrictions, passed at the state level, limit school district spending and the amount of revenue that can be raised at the local level to meet the needs of schools.

10. Will this be a windfall for schools?

While LB 280 creates a new revenue source for all schools and increases state aid for 90 percent of districts, it also reduces the maximum levy that schools can charge for property taxes, while leaving in place existing restrictions on school budget growth. Because of these levy and spending limitations, no district could use the school-funding surtax revenue or state aid increase to dramatically increase their spending, which means the vast majority of increased revenue will translate directly into property tax reductions. Some districts may choose to raise additional revenue through the school-funding surtax to increase spending but can only do so up to the amount allowed under the existing limitation on spending growth.

11. Will this take funding away from students in high poverty districts? Furthermore, will this mean more money for some school districts? If so, which districts can expect a boost in funding?

This plan is revenue neutral for school districts, and no district will lose overall funding under this proposal. Some districts that have large amounts of income wealth — which is currently not taxable for local schools or considered in the state aid formula — will see reduced state aid as a result of making their income wealth taxable and including it in their resource calculation. High poverty districts such as those in urban areas may see a different mix of income tax, property tax, and state aid, but they will not lose funding overall. In fact, giving districts access to currently untapped income wealth will improve high poverty districts’ ability to protect their schools from cuts in the event of a drop in agricultural land values or other shift in state aid. (View examples of how this proposal would impact 4 school districts.)

12. How does the per-student aid component work in LB 280?

Every district receives $500 per formula student under this proposal. The per-student aid is included as a resource in the TEEOSA formula. It is not reduced by the minimum levy adjustment. Some districts may not receive equalization aid in addition to the per-student aid, but total state aid to each district will not drop below the $500 per formula student amount.

Download a printable PDF of these questions. Go to main LB 280 FAQ page or read about the bill’s impact on taxpayers.